Legacy Planning Checklist

You have worked hard not only to build wealth but also to build memories. The families we work with want to make sure their assets are properly respected while they are being used for their own needs as well as their financial heirs.

Financial Enhancement Group works diligently to make sure assets are properly titled, properly owned, and prepared for simplicity of transfer when the time is right.

I. In a perfect world what would you want your legacy to look like?

- Assets (Everything you own or have rights to)

- Real Property

- Anticipated inheritances

- Special circumstances (handicapped children, marital issues, etc.)

- Included updated list of assets

- Letter of instructions

- Advisors to call

- Passwords for electronics

- Special gifting instructions

- Burial instructions

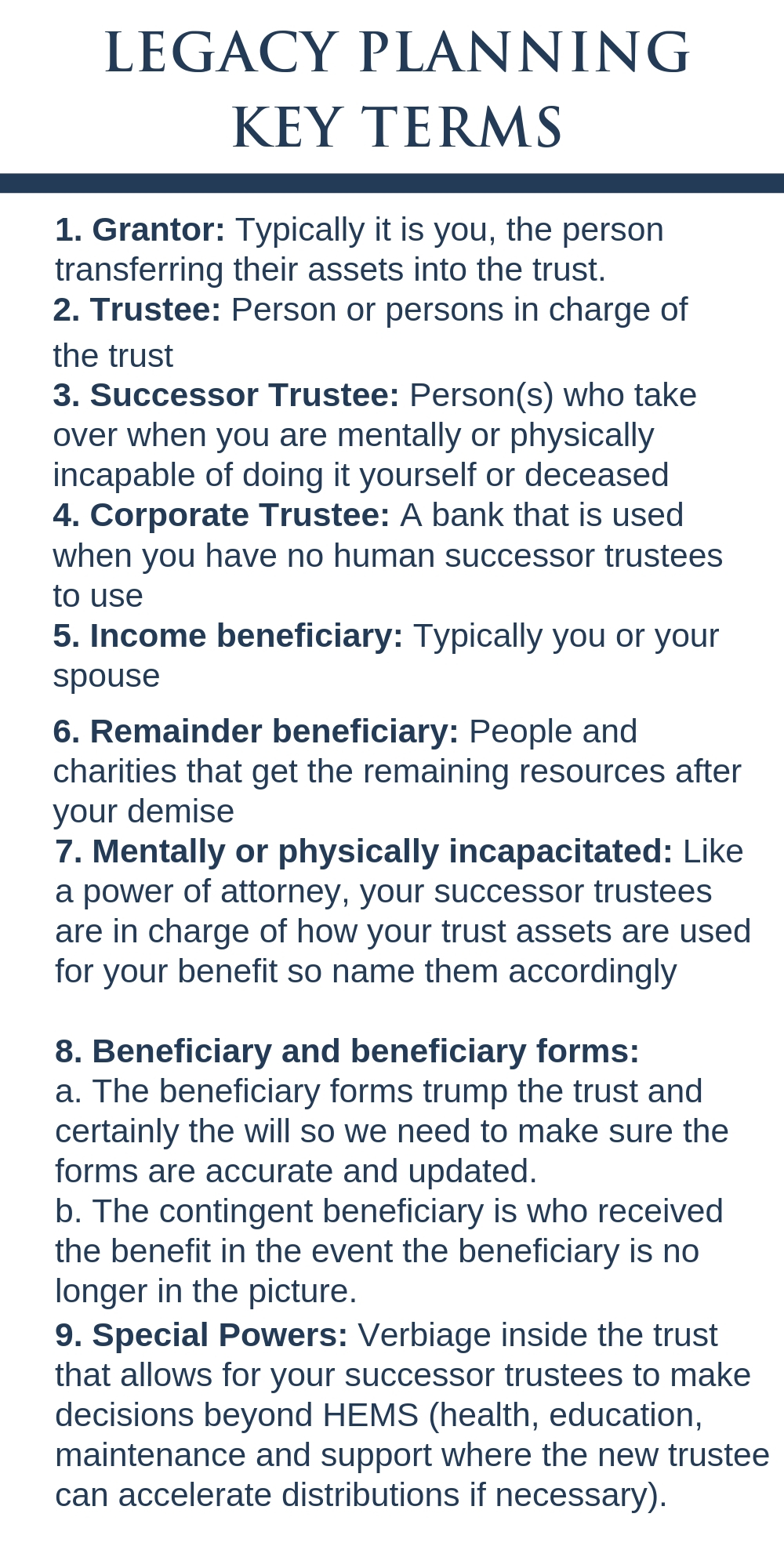

II. Trustees

A. I prefer humans, not banks, and in odd numbers so there is never a stalemate requiring a court action to break the argument.

B. In my opinion they should never be people who are recipients of the assets when you are gone. Conflicted interest by definition.

III. Trust Protector

A. Decanting Possibilities: recent addition to Indiana code but allows for the trust to be changed (not beneficiaries) for updating with changing tax codes.

B. This can be the trustee or it can be the trust protector.

C. If I am the trust protector it is me individually not the firm. I have the right to hire and fire corporate trustees if they ever need to be used and the ability to take the trust for updating when necessary and allowed.

IV. Funding the trust (what goes in and what does not)

Transferring deeds, titles, business ownership interests and beneficiary docs to the trust (Typically not retirement assets)

V. IRA’s and 401k’s (Retirement Plans)

A. These assets need to go to a living breathing person in order to delay the taxation through a process called “the stretch.” This allows your heirs to take money out over their life expectancy.

B. When this amount is larger than what you would like to leave to a beneficiary without restriction we can create a specialized trust.

VI. Distributions to other beneficiaries

A. I prefer that they need to be 30 to get any and then 1/3rd upon the last living beneficiary’s demise. Five years later another 1/3 and five years later they have control of the rest. They can chose to leave it in the trust but they have the control to do whatever they chose.

B. This gives the heirs three chances to mess up

C. This helps protect the other two disbursements from becoming marital property (There is no guarantee here as it depends on the judge and council BUT you have a much better chance of maintaining the asset in the family in the event of a divorce.)

VII. Distributions to spouse

A. If they don’t get complete control over the trust at the other spouses demise, then some of the assets can go to a family trust. The surviving

spouse gets all the income every year or 5% of the principal if that is more than the income.

B. In my trust Barb maintains some in her trust but I also use a family trust to protect assets so that some get to my daughters.

C. There is no longer need for two trust for estate tax purposes. The Portability allowance protects states above $10.5 million at this point and increasing with inflation. I use the two trust scenario for other reasons.

VIII. Other necessary Docs

A. Pour over will

B. Healthcare Representative

C. Advanced healthcare directive

D. Financial Power of Attorney

E. HIPPA release form